Telegram

Telegram Fintech Software Development Company

Helping businesses achieve their goals for over 10 years. Building apps that make profit. Attracting paying customers.

- Apps Development

- Cryptocurrencies and Blockchain

- Web3 and DeFi platforms

- Influencer Marketing

- PR and Media

- Community Management

Our Services

We develop web and mobile applications, conduct effective marketing campaigns. How to immerse yourself in all the variety of services and understand what kind of set you need? Let's start with concept development!

Fintech Development Services

We develop for fintech: mobile banking, payment systems, and crypto projects (blockchain apps, crypto wallets, crypto trading platforms, DeFi, and Web3).

Fintech Marketing Agency

Everything you need to promote and drive traffic: influencers and bloggers, PPC advertising, SEO for crypto projects, community management, PR and media.

Mobile App Development

Development of cutting-edge mobile applications for iOS and Android. Artificial intelligence, highload, nice and user-friendly design of mobile applications - that's about us

Listing and Market Making Services

Marketmaking is the process of market formation and trading for a cryptocurrency. It consists of two parts: listing on a crypto exchange and filling order books with liquidity, as well as managing the rate.

Mobile Banking App Development

Development of functional mobile banking systems that can become a powerful driving force for your business.

Cryptocurrency Wallet Development

Development of custodial and non-custodial crypto wallets with a user-friendly interface for any platform (web, desktop and mobile wallets).

Cryptocurrency Exchange Development

Development of decentralized and centralized cryptocurrency exchanges, exchangers and P2P platforms with a modern design and flexible functionality.

Recent Cases

GigaEx Case Study

Development of a centralized GigaEx exchange with the ability to replenish with fiat currencies and support for its own exchange token for use in specialized sections of the exchange.

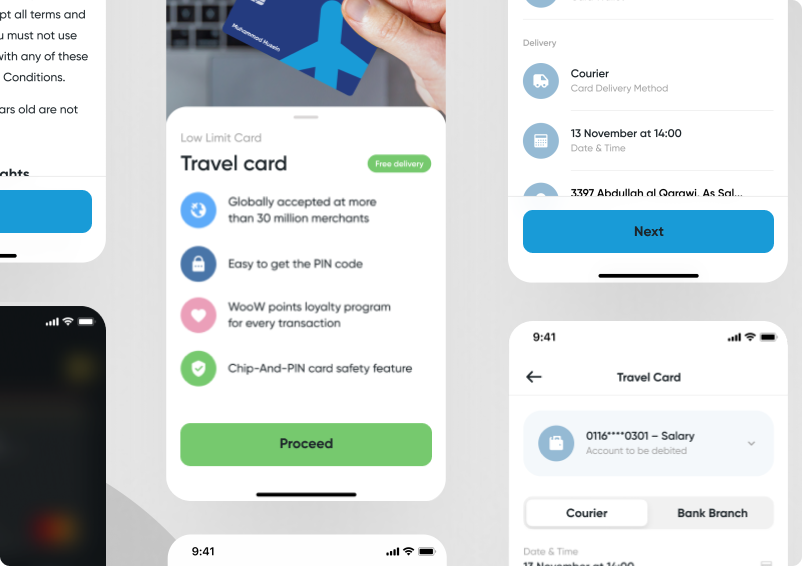

PROMT Case Study

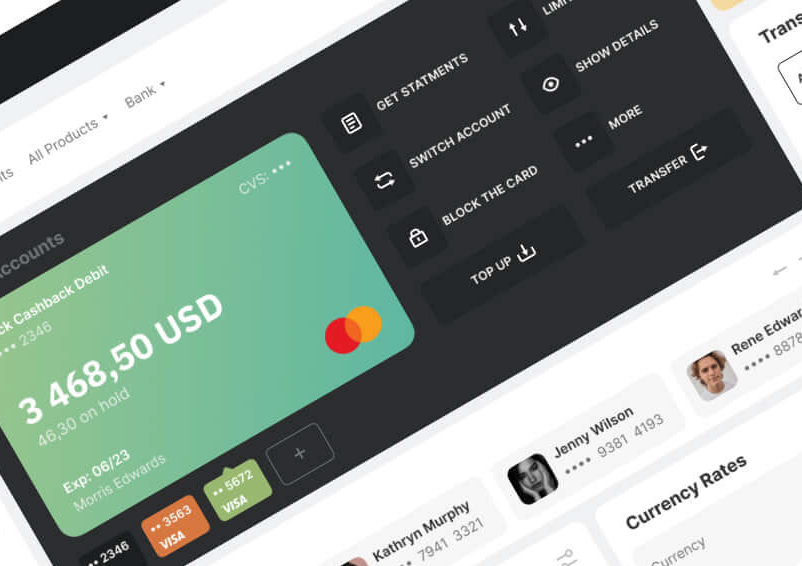

Promt is an online bank that provides banking services in the European Union. From banking services, these are accounts with the option of currency conversion, debit cards, virtual cards.

CONF Coin Case Study

Listing of the CONF Coin token on centralized cryptocurrency exchanges with full information support up to the launch of trading and subsequent support.

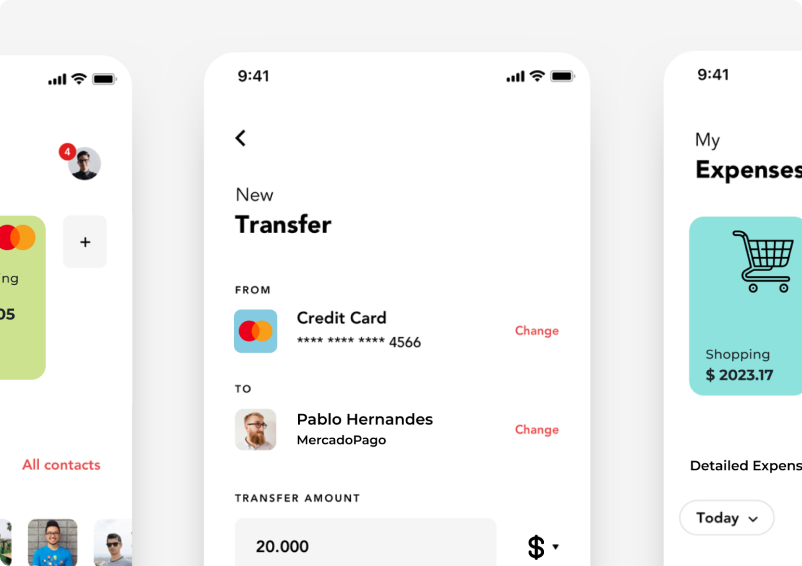

EMI PayWay Case Study

PayWay is an electronic wallet that was developed by our team on request. Users can send and receive payments worldwide, and use it to store fiat currencies and cryptocurrencies.

Cryptex Coin Case Study

Development of the Cryptex Coin cryptocurrency with its own blockchain, a JSON-RPC management interface for interacting with the main platform.

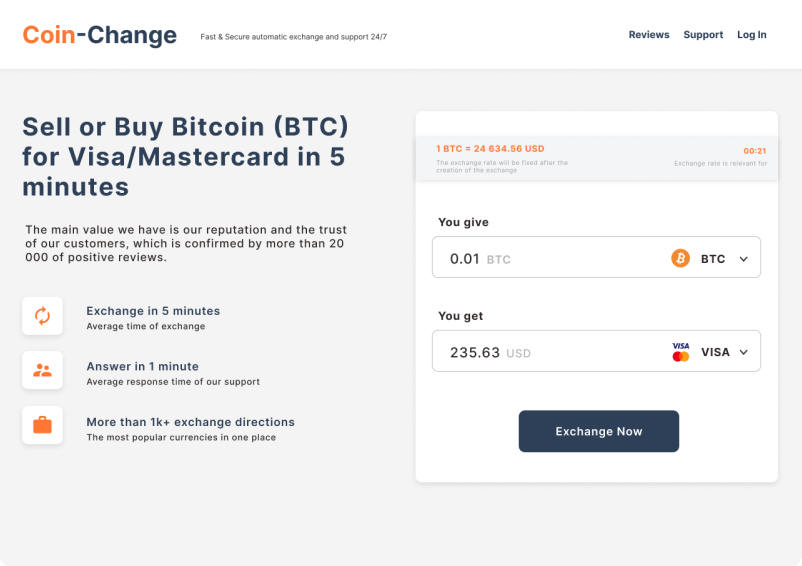

Coin-Change Case Study

Coin-Change is a modern and convenient service developed by our team for our client that allows you to quickly and safely exchange cryptocurrency in automatic mode.

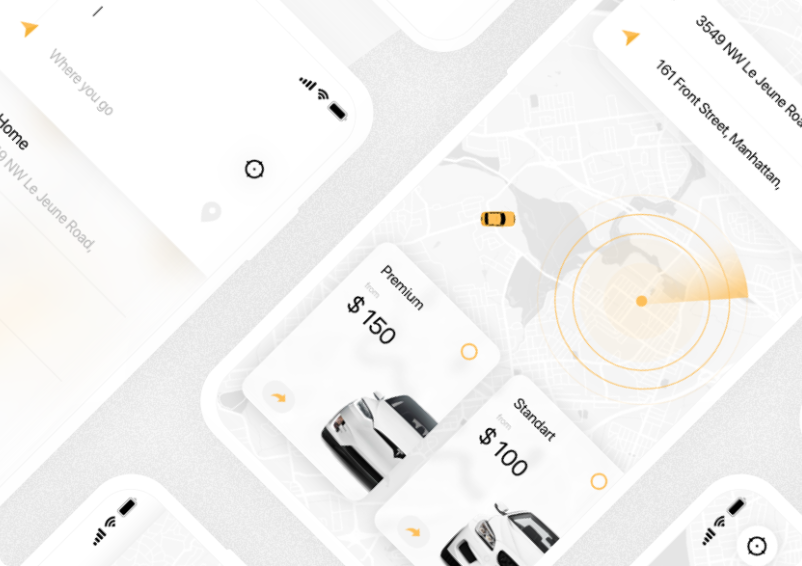

E-Taxi App Case Study

E-Taxi is a US company that provides taxi services. At the time of contacting us, the company was a start-up that received a grant from the government to create one of the first eco-friendly taxi services.

FITTY Coin Case Study

Maintaining the exchange rate and liquidity of the FITTY Coin cryptocurrency in a stable price range on the exchange, filling the order book and maintaining a low spread.

NOXE BANK Case Study

Noxe Bank is a commercial bank focused entirely on remote customer service. The main products for individuals are credit and debit cards, as well as deposits.

Finrex Token Case Study

Development of the Finrex Token on two blockchains for an ecosystem consisting of a cryptocurrency exchange, a mobile wallet and a launchpad.

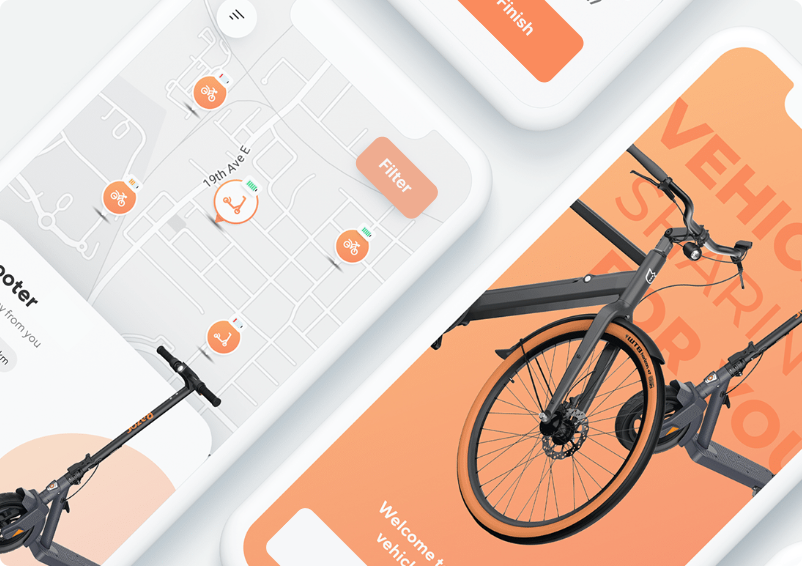

Woozz App Case Study

Woozz is a Nordic company that was one of the first in its country to launch an electric scooter rental service.

Smart Home Logic App Case Study

Smart Home Logic is a company specializing in the production of components for smart devices for smart home control.

OLA BANK Case Study

We were approached by a client with the task of developing a mobile banking application for a bank that became part of the client's group of companies. The client's core business is a regional Latin American marketplace.

ALPHA ONE Case Study

We were approached by a client with a request to develop a mobile application for their own subsidiary, a neobank entering the MESA market.

DEF Coin Case Study

Market making of DEF COIN cryptocurrency. Regulation of offers on the exchange to maintain a given rate in order to increase the popularity of the coin.

Direct Access to Most Reliable Resources

Media and Press

YouTube

Dear Customers About Us

We approached with the task of developing a DEX exchange and received quite comprehensive information on the entire development process, cost, timing, and a brief tour of the DeFi world. They quickly agreed and got to work. The exchange was done quickly and efficiently, I really liked that they quickly respond to any questions and also quickly resolve them and provide feedback. More than once they were contacted for our other projects. Recommended!

We needed help listing cryptocurrencies on centralized exchanges. Tried both ourselves and through different companies, but overpriced and uncertain. implemented in Polygant without much hope! After the first contact, we received an adequate offer for the cost and time of listing on 3 exchanges from the top 20 CoinmarketCap. They did everything clearly on time, helped with the preparation of legal documents, the conclusion of the process of contracts with exchanges and controlled all the technical input of our coin documentation to the exchange. We recommend their listing services on cryptocurrency exchanges.

As a client of Polygant, I would like to express my sincere joy and satisfaction with the cooperation in the development of a cryptocurrency exchange. They exceeded all our expectations. From the very first contact, we listened carefully to our needs and ensured careful planning of each stage of development, making an exchange that combines security, intuitiveness and high performance. Your team is living up to its reputation as cool professionals in the field of fintech development.

We recently launched a crypto exchange and knew that effective online marketing would be the key to our success. Therefore, we turned to the Polygant team for help. Their team of experts has developed a comprehensive strategy that includes a range of tactics from social media advertising to email marketing. The campaign was a huge success and as a result we saw a significant increase in both traffic and user registrations. I highly recommend Polygant for any digital marketing needs, especially in the crypto space.

We have our own token and we addressed the problem that our chart on the exchange looked broken and trades were quite rare. We wanted the token rate to remain in a stable price range and, when selling or buying, the price did not go beyond it. – with which the Polygant team successfully coped. They helped us with the release of the token to a stable exchange rate and liquidity in trading pairs on the exchange. This solved the issue of trust in the token and attracted many new holders. If you have problems with trading or the rate of the token, then these guys are definitely for you, they know their stuff!

Very happy with our partnership with Polygant to bring AI to our marketplace to predict user preferences and recommend products. Their team has extensive experience with AI and a deep understanding of the client’s goals and concerns. With their help, sales on our platform grew by almost a third after only a month of implementation. Further growth exceeded our expectations 🙂

I recently worked with the Polygant team to develop a mobile wallet for our cryptocurrency and I am very pleased with the result. The team was extremely knowledgeable and efficient in their approach and they were able to deliver a high quality product in a very short time frame. The wallet is a huge hit with our users and we’ve received a lot of positive feedback about its functionality and ease of use. I highly recommend Polygant for any mobile wallet development.

When we planned to launch our token, we initially understood that influencers would be a key part of our promotion strategy. Therefore, we turned to Polygant for help. Their team has extensive industry experience and a deep understanding of how to effectively reach our target audience through partnerships with LOMs. They were able to identify and attract bloggers with huge audiences and the campaign was a huge success. I highly recommend Polygant to anyone who wants to harness the power of influencers in the crypto space.

We are a traditional financial institution and are just entering the world of cryptocurrencies. We understand that we need a strong PR strategy to deliver our message effectively and build trust in this space. Therefore, we turned to Polygant for help. Their team has extensive experience in the crypto industry and a deep understanding of the media landscape. They have been instrumental in positioning us as thought leaders and have helped us secure top-tier media exposure. We are very pleased with the results of our partnership with Polygant and highly recommend their public relations services to any business looking to succeed in the crypto world.

I am very pleased with the results of our partnership with Polygant to promote our new crypto token. From the very beginning, their team has been incredibly professional and proactive in understanding our goals and developing a comprehensive strategy to reach our target audience. They executed this plan with exceptional attention to detail. As a result, everything flooded so much that we did not even expect :).

Polygant quickly understood our business problem and came up with an effective, high-quality solution. Not only we received a premium product for our clients, but also felt strongly positive about the development experience. We’ll definitely reach out to them in the near future.

Our restaurant chain reached out to the Polygant team with the task of creating an official HR portal. They impressed us with a responsible approach to business and a deep attention to the task. We received a ready-made portal precisely in time, which allowed us to increase the number of applicants exponentially.

We selected Polygant following a competitive tender, and were delighted by the team’s dedication and approach, delivering a great product in tight timelines and within budget. The implication and the high technical quality of their work makes Polygant a perfect partner for successful projects.

Feel Free to Contact Us

Polygant is a leading fintech software development company that specializes in providing innovative fintech software development services.

Polygant excels in fintech software development by leveraging the latest technologies and industry best practices to create scalable and secure solutions. Our team of talented fintech software developers possesses deep expertise in crafting tailored solutions that address the unique challenges faced by our clients.

Polygant’s services cater to various entities in the financial industry, including financial institutions, fintech startups, and software vendors. We are a trusted partner for all fintech software development needs.

Polygant offers a comprehensive range of fintech software development services, including financial software development services, custom software development services, fintech mobile app development services, and consulting services.

Polygant has extensive experience working with financial institutions and offers specialized solutions tailored to meet their unique needs. Our financial software development services empower banks, credit unions, and other financial organizations with scalable and secure software solutions.

Polygant understands the dynamic nature of the fintech industry and provides agile and innovative solutions to fintech startups. We assist in developing cutting-edge software solutions that help startups differentiate themselves and stay ahead of the competition.

Polygant specializes in fintech mobile app development, creating feature-rich and user-friendly mobile banking apps. Our mobile banking apps provide intuitive and convenient solutions, enhancing customer engagement.

Yes, Polygant provides consulting services to help businesses make informed technology decisions. Our consulting services encompass technology roadmapping, system integration, and digital transformation initiatives, leveraging our industry knowledge and experience.

Polygant develops advanced document management systems for financial institutions to streamline processes, enhance security, and improve collaboration. Our solutions optimize operational efficiency and ensure compliance with regulatory requirements.

Polygant actively collaborates with fintech startups, offering tailored fintech software development services to support their growth and success. We help startups bring their innovative ideas to life and revolutionize the industry.

Polygant focuses on digital banking and offers end-to-end digital banking solutions to enable financial institutions to embrace digital transformation. Our solutions create intuitive and secure digital banking experiences that drive customer engagement and loyalty.

Polygant’s comprehensive fintech software development services empower businesses in the financial industry to drive digital transformation, enhance operational efficiency, improve customer experience, and stay competitive in the evolving fintech landscape.

In conclusion, Polygant is a leading fintech software development company that offers comprehensive solutions to the financial industry. Our team of talented fintech software developers provides innovative fintech software development services, enabling success in the fintech landscape.